HABIT 004: BUILD CREDIT, NOT DEBT.

— “Beware of little expenses; a small leak will sink a great ship.”

~Benjamin Franklin

Having a High Credit Score opens up huge doorways of opportunity for the future. Business ideas, free travel, major purchases… but first and foremost, it’s important to build or rebuild credit.

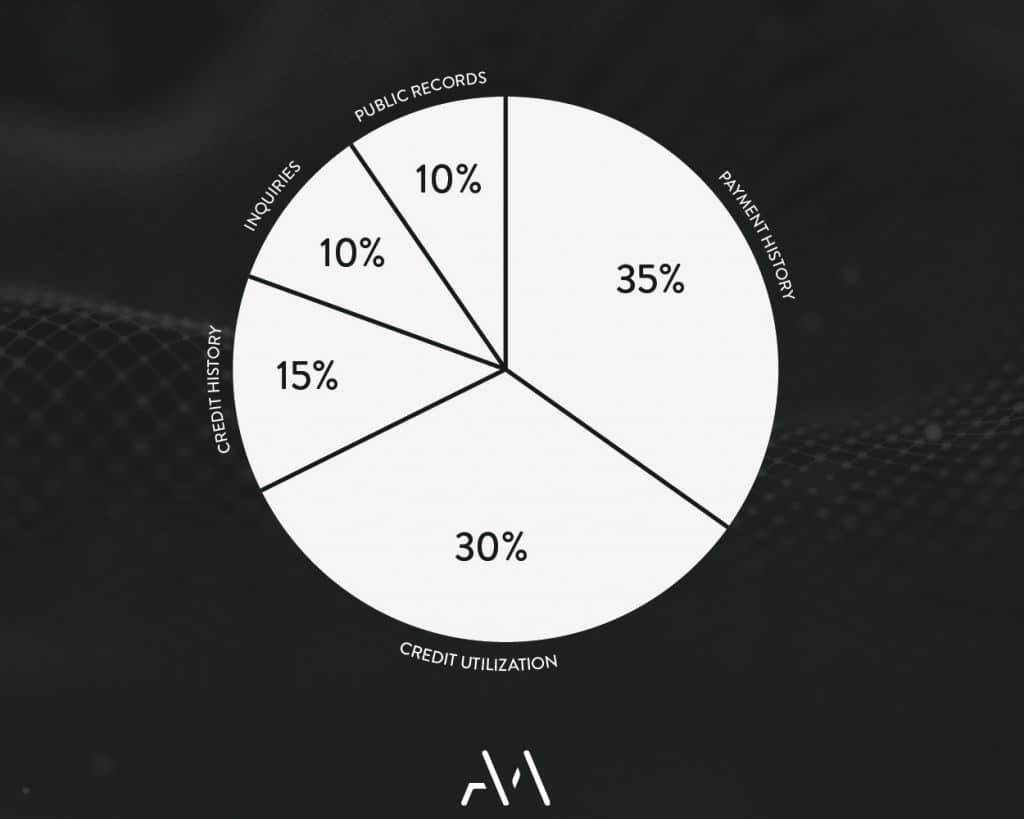

CREDIT SCORE BREAKDOWN

(from most to least important)

Payment History – 35% Credit Utilization – 30% Credit History – 15% Public Records – 10% Inquiries – 10% SIMPLE WAYS TO CORRECT CREDIT USE FOR CREDIT SCORE IMPROVEMENT

Payment History is an obvious one and makes up 35% of the score. Do not miss a payment! Use an app. Find a way to automate the process or at very least set an early reminder. Credit Utilization is important to keep it low but not 0. The purpose of a credit score is to gauge the likelihood that someone will repay the money they borrow. Higher balances are more difficult to afford and could indicate over extension. Use under 20% of the credit limit before paying it off. Do not wait until the monthly statement comes in. In a perfect situation use under 10%. If the payment frequency becomes a headache due to a low card limit, ask the creditor for an increase. This will also drop the utilization ratio to a more manageable amount. An alternative to this would be to spread out charges over multiple cards instead of one card, especially if there is a large payment. A low maintenance method for those not wanting to aggressively grow credit is to simply pay cards weekly or bi-weekly. Credit History. Do not cancel cards or bank accounts. Swap them out for low-fee or no-fee alternatives and stow them away instead. The longer the credit is held, the more trusted it is. Inquiries. Limit credit inquiries to absolutely no more than 6 hard inquiry periods per year. The likelihood of credit approval drops by doing too many. Credit Diversity. Car-Loans, Mortgage, Line of Credit, Credit Cards…the more responsible someone is with more different types of credit the more appealing that person is to lenders.

LASTLY 2 FREE WAYS TO MONITOR YOUR CREDIT SCORE ACROSS BOTH CANADIAN PLATFORMS:

—

Love the content? +Invite a friend or two while membership is open!